Applying for immigration benefits for the first time can feel overwhelming, when you are unsure about the process or the […]

Popular Posts

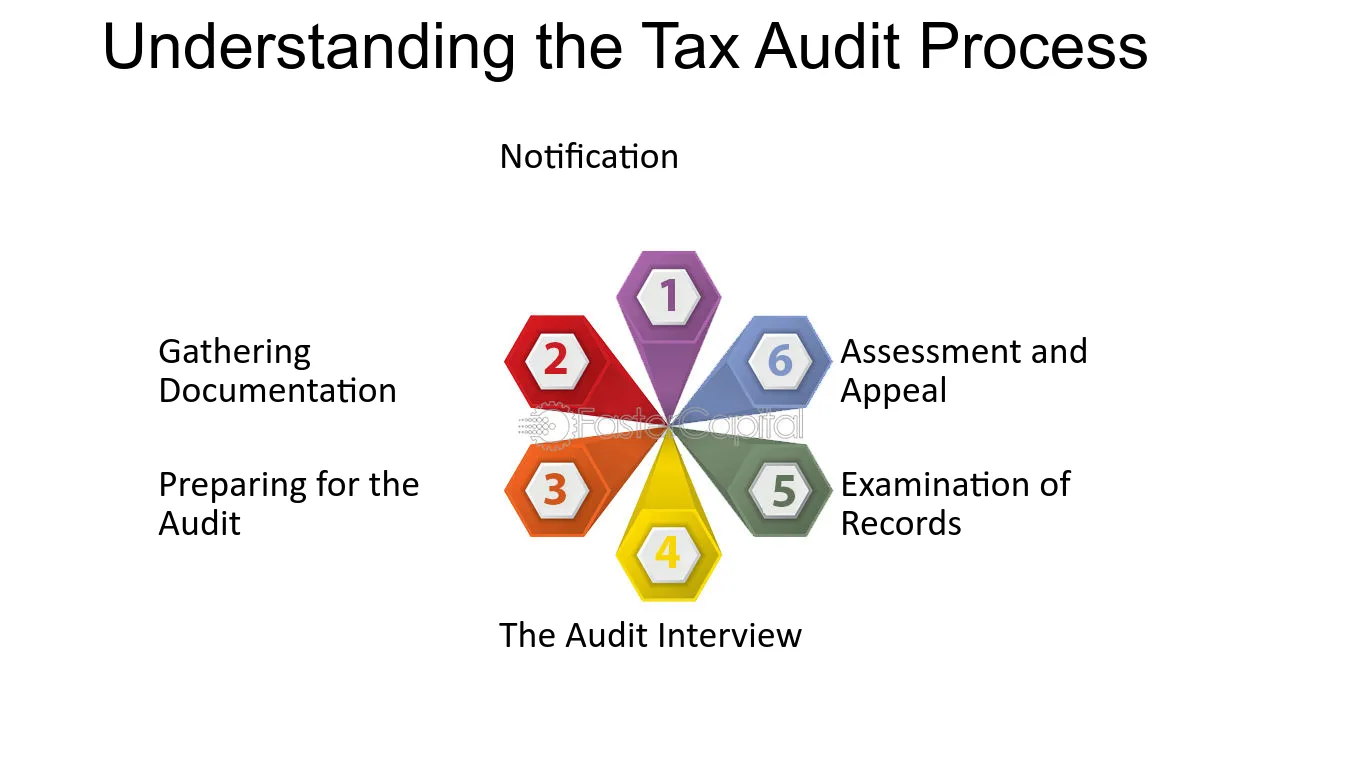

What are the methods of tax audit?

Methods of Tax Audit: A Comprehensive Guide Tax audits are a fundamental part of any nation’s tax administration system. They […]

What is the formula for spousal support in Ontario?

Spousal support in Ontario is calculated using the Spousal Support Advisory Guidelines (SSAG), which provide two main formulas: one for […]

What is the Most a VA Disability Lawyer Can Charge?

What is the Most a VA Disability Lawyer Can Charge? Introduction Navigating the complexities of VA disability claims can be […]

How Long Can You Leave Spider Plant Babies in Water?

Spider plants, scientifically known as Chlorophytum comosum, are one of the most popular and easy-to-grow houseplants. They are known for their […]

Can I Spray Rubbing Alcohol On Plants?

Understanding Rubbing Alcohol Rubbing alcohol, also known as isopropyl alcohol, is a common household item used for various purposes, including […]

Can Spider Plants Grow In Just Water?

Can Spider Plants Grow in Just Water? A Guide to Water Propagation Spider plants (Chlorophytum comosum) are known for their […]

What Happens If You Bury An Egg And A Banana?

A Backyard Science Experiment: Burying Eggs and Bananas – Unveiling Decomposition and Gas Our backyards are brimming with opportunities for […]

Simple Home Decor Ideas to Transform Your Space!

Decorating a home sounds exciting, doesn’t it? But when you actually get down to it, it can feel a bit […]

What to Expect at Your First Dentist Appointment

Visiting a new dentist for the first time can feel overwhelming, especially if you don’t know what to expect. Whether […]